Wireless BIG 5, 4, 3, 2……..?

In the wireless world, we had the BIG 5 – AT&T Mobility, Verizon Wireless, Sprint/Nextel, T-Mobile and Alltel. After the purchase of Alltel by Verizon Wireless, the BIG 5 have become the BIG 4……for now. Several key issues and forces may dramatically shape the wireless landscape over the near term. What should large enterprises do now to hedge their bets regarding some potentially devastating outcomes?

Consider the following:

Over 85% of the population of the United States has a mobile device. Market saturation has been, or soon will be, reached. The mobility carriers realize the past years of double digit growth of both users and usage is coming to a close. With limited non-users to attract, the carriers’ focus shifts to feeding on each other’s base of existing users. We have seen two key events which have had a significant impact. First, the introduction and high success of the iPhone by AT&T Mobility. Recent quarterly gains have been realized at the expense of Sprint and T-Mobile. Second, the purchase of Alltel by Verizon Wireless has taken a key player out of the market and propelled the combined company to #1 in terms of total subscribers. This has provided bragging rights to Verizon Wireless and, with their introduction of the Storm, helped counter the iPhone impact to their embedded base.

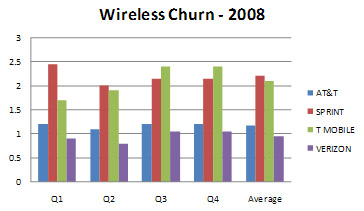

Sprint/Nextel actually lost subscribers during the past year due to the above mentioned iPhone impact coupled with a history of poor customer service. They are facing a critical and difficult year ahead. The potential outsourcing of their network operations is drawing mixed reviews. A stated focus on improving customer service may deliver the necessary improvements to quell the high churn rate but results remain to be seen by the consumer and business customers. They are currently betting the farm on the success of the Pre to move them back to a positive subscriber gain environment. The possibility of Sprint/Nextel being purchased (perhaps by a cable company such as Comcast) is stronger than ever before and may be their only path available if a return to profitability is not reached by 2010.

T-Mobile also experienced less growth over the past year with their average churn rate increasing to above 2.1%. They are still plagued by coverage perception and reality issues. Always the lowest cost provider in the past, T-Mobile will continue that strategy as evidenced by the announcement of the lowest cost unlimited plans currently in the market. With strong financial backing from parent company, Deutsche Telekom, T-Mobile should survive near term but will likely remain in their current role as a secondary or niche provider for enterprises.

What strategy should large enterprises consider?

Currently most large wireless users (i.e. 1000 devices and above) have what looks like a diversified investment portfolio made up of four to ten carriers with a broad mixture of market share, devices, monthly plans and features. Consider consolidating to one of the following models:

1. Consolidate to enhance volume discounts and buying power: Select a Primary provider for 80% to 90% of devices with most, or all, future devices ordered from them. Select a Secondary carrier for the majority of the non-primary devices and serves the role of fallback carrier for those who have coverage issues or other circumstances preventing them from using the Primary. Transition to the selected distribution may occur over time via a well managed conversion process to avoid unnecessary disruptions and early termination fee expenses.

- If the Primary is Verizon Wireless or AT&T Mobility and the Secondary is the other one, consider an ~80%/20% mix.

- If the Primary is Verizon Wireless or AT&T Mobility and the Secondary is Sprint/Nextel or T-Mobile, consider a ~90%/10% or even a 95%/5%mix.

- If the Primary is Sprint/Nextel or T-Mobile, the Secondary should always be AT&T Mobility or Verizon Wireless with a mix at something less than 80% and even approaching 50% for the Primary. In this case, consider multiple Secondary providers.

2. Data capabilities key to future productivity applications: Evaluate the current and future state of each provider’s data network performance, availability and reliability (PAR). Utilize metrics and evaluation criteria to determine a PAR score for each provider considered for critical applications and for critical locales/population areas.

3. Understand the wireless device current inventory: Compile, or have a third party compile, a complete inventory from the various providers’ billing media. Complete with device type, plan type, usage and features information, this inventory will provide the basis for sourcing and consolidation activities. It will also uncover potential areas for additional cost savings (zero minute users, multiple devices for single users, usage trends, monthly minute plan adjustments, etc.).

4. Conduct a sourcing event: Utilize professional consulting services specialized in wireless contract negotiations. Competitive sourcing, along with market place knowledge and benchmarking of current pricing, provides greater results for cost savings through lower pricing, higher discounts and additional credits. Best in Class contractual terms and conditions will also provide on-going governance and flexibility to the enterprise. The selection of a Wireless Expense Management provider should also entail a competitive sourcing process and may often be incorporated into the initial provider sourcing event or any contract re-negotiation activities.